David Edelman – författare

Visar alla böcker från författaren . Handla med fri frakt och snabb leverans.

6 produkter

6 produkter

Häftad, Engelska, 2019

1 005 kr

Skickas inom 10-15 vardagar

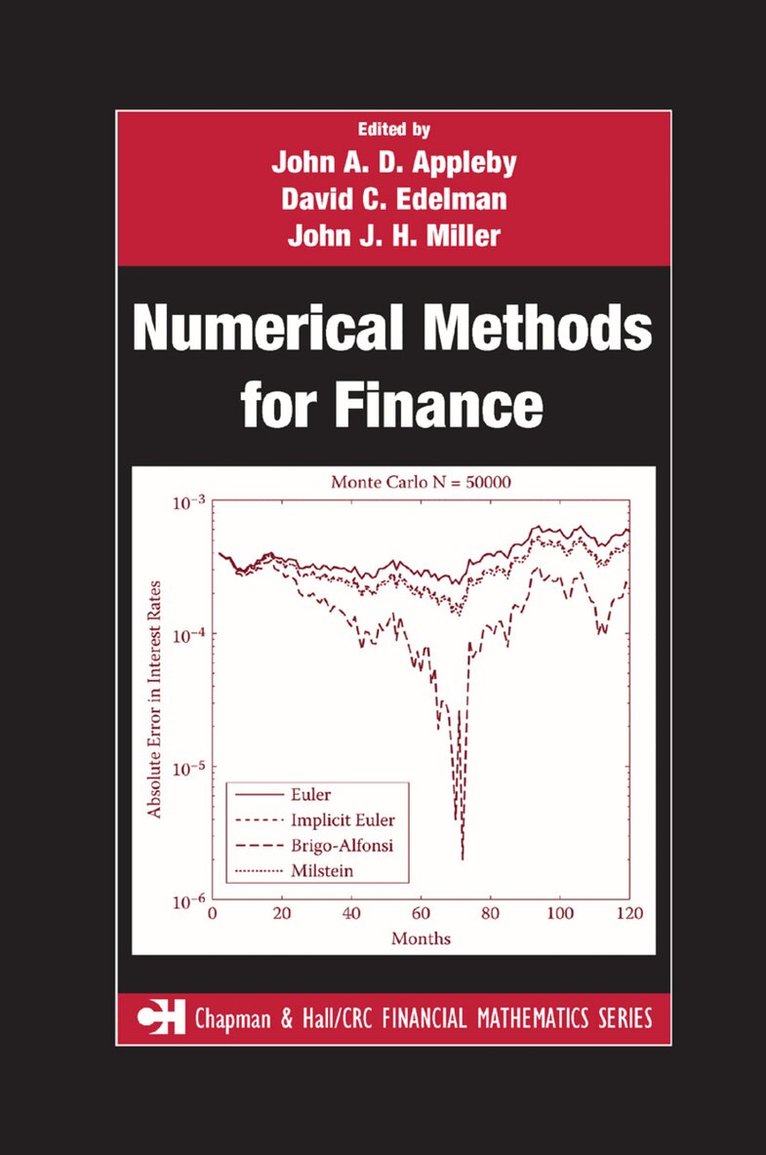

Featuring international contributors from both industry and academia, Numerical Methods for Finance explores new and relevant numerical methods for the solution of practical problems in finance. It is one of the few books entirely devoted to numerical methods as applied to the financial field.Presenting state-of-the-art methods in this area, the book first discusses the coherent risk measures theory and how it applies to practical risk management. It then proposes a new method for pricing high-dimensional American options, followed by a description of the negative inter-risk diversification effects between credit and market risk. After evaluating counterparty risk for interest rate payoffs, the text considers strategies and issues concerning defined contribution pension plans and participating life insurance contracts. It also develops a computationally efficient swaption pricing technology, extracts the underlying asset price distribution implied by option prices, and proposes a hybrid GARCH model as well as a new affine point process framework. In addition, the book examines performance-dependent options, variance reduction, Value at Risk (VaR), the differential evolution optimizer, and put-call-futures parity arbitrage opportunities.Sponsored by DEPFA Bank, IDA Ireland, and Pioneer Investments, this concise and well-illustrated book equips practitioners with the necessary information to make important financial decisions.

Inbunden, Engelska, 1986

2 224 kr

Skickas inom 10-15 vardagar

E-bok

Engelska, 20071 194 kr

Läs direkt efter köp

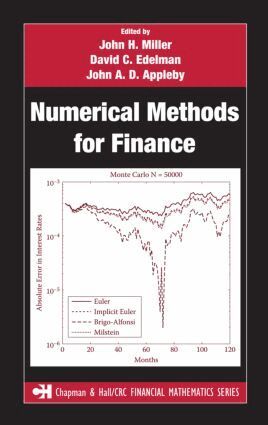

Featuring international contributors from both industry and academia, Numerical Methods for Finance explores new and relevant numerical methods for the solution of practical problems in finance. It is one of the few books entirely devoted to numerical methods as applied to the financial field.Presenting state-of-the-art methods in this area

Inbunden, Engelska, 2007

2 959 kr

Skickas inom 5-8 vardagar

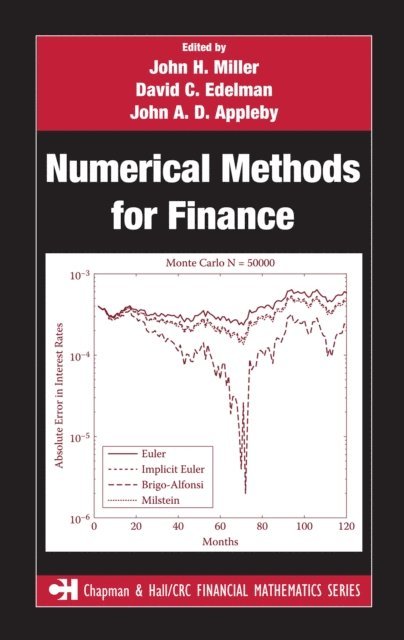

Featuring international contributors from both industry and academia, Numerical Methods for Finance explores new and relevant numerical methods for the solution of practical problems in finance. It is one of the few books entirely devoted to numerical methods as applied to the financial field.Presenting state-of-the-art methods in this area, the book first discusses the coherent risk measures theory and how it applies to practical risk management. It then proposes a new method for pricing high-dimensional American options, followed by a description of the negative inter-risk diversification effects between credit and market risk. After evaluating counterparty risk for interest rate payoffs, the text considers strategies and issues concerning defined contribution pension plans and participating life insurance contracts. It also develops a computationally efficient swaption pricing technology, extracts the underlying asset price distribution implied by option prices, and proposes a hybrid GARCH model as well as a new affine point process framework. In addition, the book examines performance-dependent options, variance reduction, Value at Risk (VaR), the differential evolution optimizer, and put-call-futures parity arbitrage opportunities.Sponsored by DEPFA Bank, IDA Ireland, and Pioneer Investments, this concise and well-illustrated book equips practitioners with the necessary information to make important financial decisions.

E-bok

PDF, Engelska, 20071 194 kr

Läs direkt efter köp

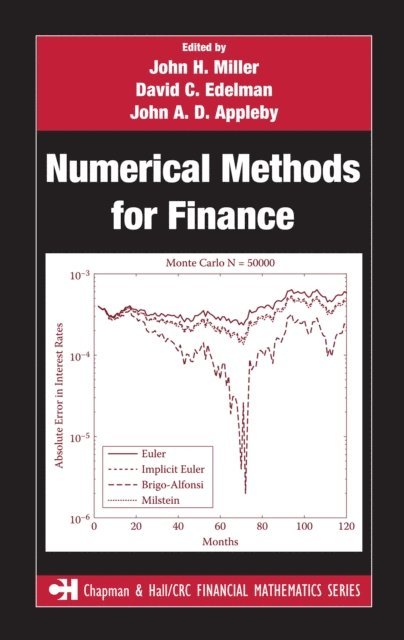

Featuring international contributors from both industry and academia, Numerical Methods for Finance explores new and relevant numerical methods for the solution of practical problems in finance. It is one of the few books entirely devoted to numerical methods as applied to the financial field.Presenting state-of-the-art methods in this area

Häftad, Engelska, 2017

1 281 kr

Skickas inom 5-8 vardagar

Credit Scoring and Its Applications is recognized as the bible of credit scoring. It contains a comprehensive review of the objectives, methods, and practical implementation of credit and behavioral scoring. The authors review principles of the statistical and operations research methods used in building scorecards, as well as the advantages and disadvantages of each approach. The book contains a description of practical problems encountered in building, using, and monitoring scorecards and examines some of the country-specific issues in bankruptcy, equal opportunities, and privacy legislation. It contains a discussion of economic theories of consumers' use of credit, and readers will gain an understanding of what lending institutions seek to achieve by using credit scoring and the changes in their objectives.New to the second edition are:lessons that can be learned for operations research model building from the global financial crisiscurrent applications of scoringdiscussions on the Basel Accords and their requirements for scoringnew methods for scorecard building and new expanded sections on ways of measuring scorecard performance, andsurvival analysis for credit scoring.Other unique features include methods of monitoring scorecards and deciding when to update them, as well as different applications of scoring, including direct marketing, profit scoring, tax inspection, prisoner release, and payment of fines.