Jean-Luc Prigent – författare

Visar alla böcker från författaren . Handla med fri frakt och snabb leverans.

11 produkter

11 produkter

E-bok

Engelska, 20073 521 kr

Läs direkt efter köp

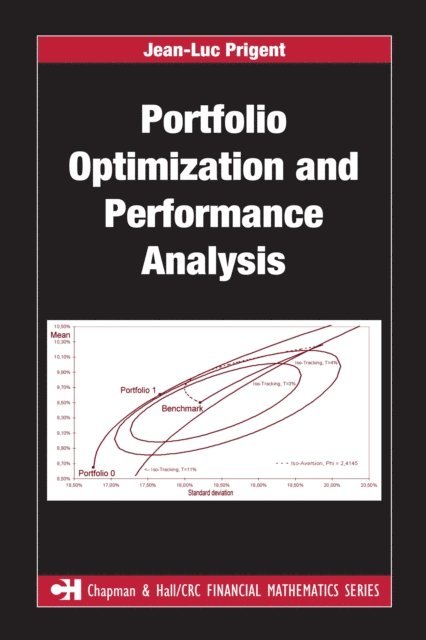

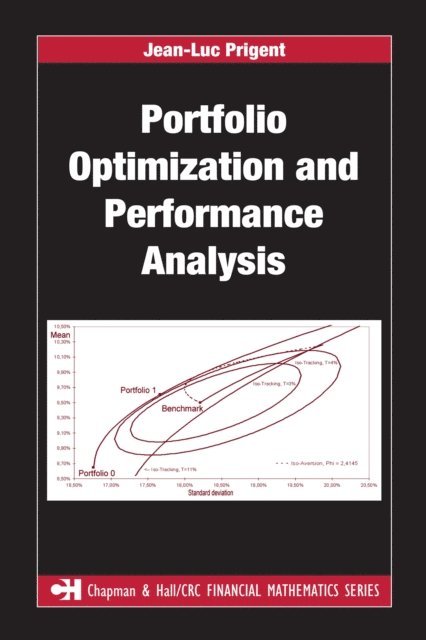

In answer to the intense development of new financial products and the increasing complexity of portfolio management theory, Portfolio Optimization and Performance Analysis offers a solid grounding in modern portfolio theory. The book presents both standard and novel results on the axiomatics of the individual choice in an uncertain framework, cont

E-bok

PDF, Engelska, 20073 521 kr

Läs direkt efter köp

In answer to the intense development of new financial products and the increasing complexity of portfolio management theory, Portfolio Optimization and Performance Analysis offers a solid grounding in modern portfolio theory. The book presents both standard and novel results on the axiomatics of the individual choice in an uncertain framework, cont

Inbunden, Engelska, 2007

3 010 kr

Skickas inom 10-15 vardagar

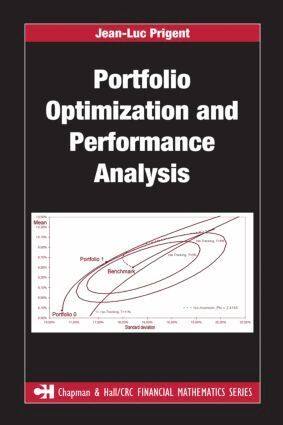

In answer to the intense development of new financial products and the increasing complexity of portfolio management theory, Portfolio Optimization and Performance Analysis offers a solid grounding in modern portfolio theory. The book presents both standard and novel results on the axiomatics of the individual choice in an uncertain framework, contains a precise overview of standard portfolio optimization, provides a review of the main results for static and dynamic cases, and shows how theoretical results can be applied to practical and operational portfolio optimization.Divided into four sections that mirror the book's aims, this resource first describes the fundamental results of decision theory, including utility maximization and risk measure minimization. Covering both active and passive portfolio management, the second part discusses standard portfolio optimization and performance measures. The book subsequently introduces dynamic portfolio optimization based on stochastic control and martingale theory. It also outlines portfolio optimization with market frictions, such as incompleteness, transaction costs, labor income, and random time horizon. The final section applies theoretical results to practical portfolio optimization, including structured portfolio management. It details portfolio insurance methods as well as performance measures for alternative investments, such as hedge funds.Taking into account the different features of portfolio management theory, this book promotes a thorough understanding for students and professionals in the field.

E-bok

PDF, Engelska, 20132 049 kr

Läs direkt efter köp

A comprehensive overview of weak convergence of stochastic processes and its application to the study of financial markets. Split into three parts, the first recalls the mathematics of stochastic processes and stochastic calculus with special emphasis on contiguity properties and weak convergence of stochastic integrals. The second part is devoted to the analysis of financial theory from the convergence point of view. The main problems such as portfolio optimization, option pricing and hedging are examined, especially when considering discrete-time approximations of continuous-time dynamics. The third part deals with lattice- and tree-based computational procedures for option pricing both on stocks and stochastic bonds. More general discrete approximations are also introduced and detailed.

Inbunden, Engelska, 2003

1 613 kr

Skickas inom 10-15 vardagar

A comprehensive overview of weak convergence of stochastic processes and its application to the study of financial markets. Split into three parts, the first recalls the mathematics of stochastic processes and stochastic calculus with special emphasis on contiguity properties and weak convergence of stochastic integrals. The second part is devoted to the analysis of financial theory from the convergence point of view. The main problems such as portfolio optimization, option pricing and hedging are examined, especially when considering discrete-time approximations of continuous-time dynamics. The third part deals with lattice- and tree-based computational procedures for option pricing both on stocks and stochastic bonds. More general discrete approximations are also introduced and detailed.

Häftad, Engelska, 2010

1 613 kr

Skickas inom 10-15 vardagar

A comprehensive overview of weak convergence of stochastic processes and its application to the study of financial markets. Split into three parts, the first recalls the mathematics of stochastic processes and stochastic calculus with special emphasis on contiguity properties and weak convergence of stochastic integrals. The second part is devoted to the analysis of financial theory from the convergence point of view. The main problems such as portfolio optimization, option pricing and hedging are examined, especially when considering discrete-time approximations of continuous-time dynamics. The third part deals with lattice- and tree-based computational procedures for option pricing both on stocks and stochastic bonds. More general discrete approximations are also introduced and detailed.

Engelska, 2012

648 kr

Skickas inom 5-8 vardagar

Inbunden, Engelska, 2023

2 543 kr

Skickas inom 10-15 vardagar

This book explores how the economic sphere has experienced an ultimate shape after the occurrence of several crises, since 2000s. The subprime crisis has trigged the transition from conventional to unconventional frameworks in most industrialised and emerging economies. This book highlights how the sovereign debt crisis has exacerbated the economic environment and raised economic uncertainty. This book asserts that markets integration have boosted contagion and risk spillovers among financial markets. Moreover, the Brexit and US-China trade tension has intensified uncertainty and the economic challenges. This book examines in recent times how humanity has experienced the most dramatic health crisis and their economic effects. This pandemic lockdowns several countries and caused an economic and financial collapse. This book expands on these crises, with different origins and mechanisms, have shaped the economic systems in several ways: monetary policy, macroeconomic imbalance, economic growth, economic integration, financial risk, volatility and trade effects.The main aims of this book cover the topical issues related to crises and uncertainty and the economic consequences. This book is drawn from academics and practitioners presenting high-quality original research papers, presented in the Financial and Economic Meeting conference 2021.

E-bok

Engelska, 20233 242 kr

Läs direkt efter köp

This book explores how the economic sphere has experienced an ultimate shape after the occurrence of several crises, since 2000s. The subprime crisis has trigged the transition from conventional to unconventional frameworks in most industrialised and emerging economies. This book highlights how the sovereign debt crisis has exacerbated the economic environment and raised economic uncertainty. This book asserts that markets integration have boosted contagion and risk spillovers among financial markets. Moreover, the Brexit and US-China trade tension has intensified uncertainty and the economic challenges. This book examines in recent times how humanity has experienced the most dramatic health crisis and their economic effects. This pandemic lockdowns several countries and caused an economic and financial collapse. This book expands on these crises, with different origins and mechanisms, have shaped the economic systems in several ways: monetary policy, macroeconomic imbalance, economic growth, economic integration, financial risk, volatility and trade effects.The main aims of this book cover the topical issues related to crises and uncertainty and the economic consequences. This book is drawn from academics and practitioners presenting high-quality original research papers, presented in the Financial and Economic Meeting conference 2021.

Häftad, Engelska, 2024

2 543 kr

Skickas inom 10-15 vardagar

This book explores how the economic sphere has experienced an ultimate shape after the occurrence of several crises, since 2000s. The subprime crisis has trigged the transition from conventional to unconventional frameworks in most industrialised and emerging economies. This book highlights how the sovereign debt crisis has exacerbated the economic environment and raised economic uncertainty. This book asserts that markets integration have boosted contagion and risk spillovers among financial markets. Moreover, the Brexit and US-China trade tension has intensified uncertainty and the economic challenges. This book examines in recent times how humanity has experienced the most dramatic health crisis and their economic effects. This pandemic lockdowns several countries and caused an economic and financial collapse. This book expands on these crises, with different origins and mechanisms, have shaped the economic systems in several ways: monetary policy, macroeconomic imbalance, economic growth, economic integration, financial risk, volatility and trade effects.The main aims of this book cover the topical issues related to crises and uncertainty and the economic consequences. This book is drawn from academics and practitioners presenting high-quality original research papers, presented in the Financial and Economic Meeting conference 2021.

Del 3 - World Scientific Studies in International Economics

Risk Management And Value: Valuation And Asset Pricing

Inbunden, Engelska, 2008

3 721 kr

Skickas inom 5-8 vardagar

This book provides a comprehensive discussion of the issues related to risk, volatility, value and risk management. It includes a selection of the best papers presented at the Fourth International Finance Conference 2007, qualified by Professor James Heckman, the 2000 Nobel Prize Laureate in Economics, as a “high level” one. The first half of the book examines ways to manage risk and compute value-at-risk for exchange risk associated to debt portfolios and portfolios of equity. It also covers the Basel II framework implementation and securitisation. The effects of volatility and risk on the valuation of financial assets are further studied in detail.The second half of the book is dedicated to the banking industry, banking competition on the credit market, banking risk and distress, market valuation, managerial risk taking, and value in the ICT activity. With its inclusion of new concepts and recent literature, academics and risk managers will want to read this book.