Qi-Man Shao – författare

1 083 kr

Skickas inom 10-15 vardagar

1 416 kr

Läs direkt efter köp

422 kr

Skickas inom 5-8 vardagar

1 083 kr

Skickas inom 10-15 vardagar

1 406 kr

Skickas inom 10-15 vardagar

1 733 kr

Läs direkt efter köp

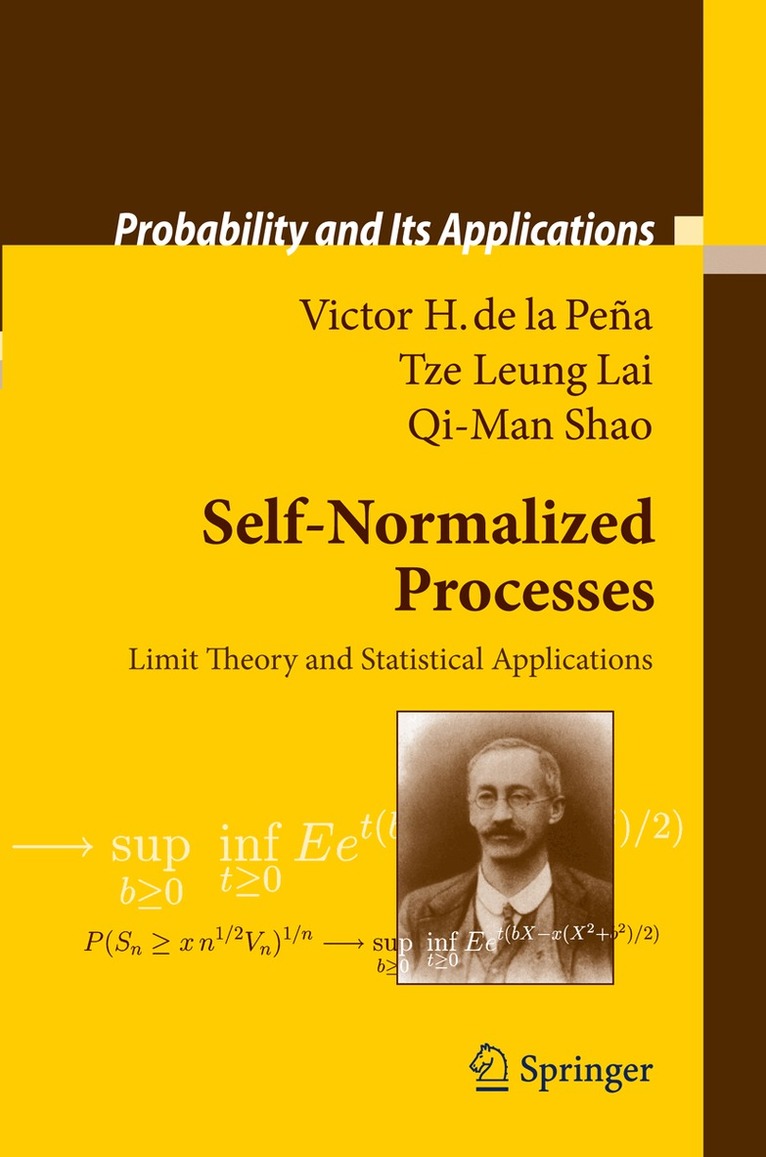

Self-normalized processes are of common occurrence in probabilistic and statistical studies. A prototypical example is Student''s t-statistic introduced in 1908 by Gosset, whose portrait is on the front cover. Due to the highly non-linear nature of these processes, the theory experienced a long period of slow development. In recent years there have been a number of important advances in the theory and applications of self-normalized processes. Some of these developments are closely linked to the study of central limit theorems, which imply that self-normalized processes are approximate pivots for statistical inference.

The present volume covers recent developments in the area, including self-normalized large and moderate deviations, and laws of the iterated logarithms for self-normalized martingales. This is the first book that systematically treats the theory and applications of self-normalization.

1 406 kr

Skickas inom 10-15 vardagar

922 kr

Skickas inom 10-15 vardagar

870 kr

Läs direkt efter köp

653 kr

Skickas inom 10-15 vardagar