Damiano Brigo – författare

767 kr

Skickas inom 10-15 vardagar

1 157 kr

Läs direkt efter köp

The book''s content is focused on rigorous and advanced quantitative methods for the pricing and hedging of counterparty credit and funding risk. The new general theory that is required for this methodology is developed from scratch, leading to a consistent and comprehensive framework for counterparty credit and funding risk, inclusive of collateral, netting rules, possible debit valuation adjustments, re-hypothecation and closeout rules. The book however also looks at quite practical problems, linking particular models to particular ''concrete'' financial situations across asset classes, including interest rates, FX, commodities, equity, credit itself, and the emerging asset class of longevity.

The authors also aim to help quantitative analysts, traders, and anyone else needing to frame and price counterparty credit and funding risk, to develop a ''feel'' for applying sophisticated mathematics and stochastic calculus to solve practical problems.

The main models are illustrated from theoretical formulation to final implementation with calibration to market data, always keeping in mind the concrete questions being dealt with. The authors stress that each model is suited to different situations and products, pointing out that there does not exist a single model which is uniformly better than all the others, although the problems originated by counterparty credit and funding risk point in the direction of global valuation.

Finally, proposals for restructuring counterparty credit risk, ranging from contingent credit default swaps to margin lending, are considered.

1 157 kr

Läs direkt efter köp

The book''s content is focused on rigorous and advanced quantitative methods for the pricing and hedging of counterparty credit and funding risk. The new general theory that is required for this methodology is developed from scratch, leading to a consistent and comprehensive framework for counterparty credit and funding risk, inclusive of collateral, netting rules, possible debit valuation adjustments, re-hypothecation and closeout rules. The book however also looks at quite practical problems, linking particular models to particular ''concrete'' financial situations across asset classes, including interest rates, FX, commodities, equity, credit itself, and the emerging asset class of longevity.

The authors also aim to help quantitative analysts, traders, and anyone else needing to frame and price counterparty credit and funding risk, to develop a ''feel'' for applying sophisticated mathematics and stochastic calculus to solve practical problems.

The main models are illustrated from theoretical formulation to final implementation with calibration to market data, always keeping in mind the concrete questions being dealt with. The authors stress that each model is suited to different situations and products, pointing out that there does not exist a single model which is uniformly better than all the others, although the problems originated by counterparty credit and funding risk point in the direction of global valuation.

Finally, proposals for restructuring counterparty credit risk, ranging from contingent credit default swaps to margin lending, are considered.

Credit Models and the Crisis

A Journey into CDOs, Copulas, Correlations and Dynamic Models

443 kr

Skickas inom 5-8 vardagar

379 kr

Läs direkt efter köp

Credit Models and the Crisis is a succinct but technical analysis of the key aspects of the credit derivatives modeling problems, tracing the development (and flaws) of new quantitative methods for credit derivatives and CDOs up to and through the credit crisis. Responding to the immediate need for clarity in the market and academic research environments, this book follows the development of credit derivatives and CDOs at a technical level, analyzing the impact, strengths and weaknesses of methods ranging from the introduction of the Gaussian Copula model and the related implied correlations to the introduction of arbitrage-free dynamic loss models capable of calibrating all the tranches for all the maturities at the same time. It also illustrates the implied copula, a method that can consistently account for CDOs with different attachment and detachment points but not for different maturities, and explains why the Gaussian Copula model is still used in its base correlation formulation.

The book reports both alarming pre-crisis research and market examples, as well as commentary through history, using data up to the end of 2009, making it an important addition to modern derivatives literature. With banks and regulators struggling to fully analyze at a technical level, many of the flaws in modern financial models, it will be indispensable for quantitative practitioners and academics who want to develop stable and functional models in the future.

Counterparty Credit Risk, Collateral and Funding

With Pricing Cases For All Asset Classes

951 kr

Skickas inom 5-8 vardagar

575 kr

Läs direkt efter köp

Credit derivatives are here to stay and will continue to play a role in finance in the future. But what will that role be? What issues and challenges should be addressed? And what lessons can be learned from the credit mess?

Credit Risk Frontiers offers answers to these and other questions by presenting the latest research in this field and addressing important issues exposed by the financial crisis. It covers this subject from a real world perspective, tackling issues such as liquidity, poor data, and credit spreads, as well as the latest innovations in portfolio products and hedging and risk management techniques.

Provides a coherent presentation of recent advances in the theory and practice of credit derivatives Takes into account the new products and risk requirements of a post financial crisis world Contains information regarding various aspects of the credit derivative market as well as cutting edge research regarding those aspectsIf you want to gain a better understanding of how credit derivatives can help your trading or investing endeavors, then Credit Risk Frontiers is a book you need to read.

366 kr

Läs direkt efter köp

Credit Models and the Crisis is a succinct but technical analysis of the key aspects of the credit derivatives modeling problems, tracing the development (and flaws) of new quantitative methods for credit derivatives and CDOs up to and through the credit crisis. Responding to the immediate need for clarity in the market and academic research environments, this book follows the development of credit derivatives and CDOs at a technical level, analyzing the impact, strengths and weaknesses of methods ranging from the introduction of the Gaussian Copula model and the related implied correlations to the introduction of arbitrage-free dynamic loss models capable of calibrating all the tranches for all the maturities at the same time. It also illustrates the implied copula, a method that can consistently account for CDOs with different attachment and detachment points but not for different maturities, and explains why the Gaussian Copula model is still used in its base correlation formulation.

The book reports both alarming pre-crisis research and market examples, as well as commentary through history, using data up to the end of 2009, making it an important addition to modern derivatives literature. With banks and regulators struggling to fully analyze at a technical level, many of the flaws in modern financial models, it will be indispensable for quantitative practitioners and academics who want to develop stable and functional models in the future.

581 kr

Läs direkt efter köp

Credit derivatives are here to stay and will continue to play a role in finance in the future. But what will that role be? What issues and challenges should be addressed? And what lessons can be learned from the credit mess?

Credit Risk Frontiers offers answers to these and other questions by presenting the latest research in this field and addressing important issues exposed by the financial crisis. It covers this subject from a real world perspective, tackling issues such as liquidity, poor data, and credit spreads, as well as the latest innovations in portfolio products and hedging and risk management techniques.

Provides a coherent presentation of recent advances in the theory and practice of credit derivatives Takes into account the new products and risk requirements of a post financial crisis world Contains information regarding various aspects of the credit derivative market as well as cutting edge research regarding those aspectsIf you want to gain a better understanding of how credit derivatives can help your trading or investing endeavors, then Credit Risk Frontiers is a book you need to read.

3 062 kr

Skickas inom 5-8 vardagar

935 kr

Läs direkt efter köp

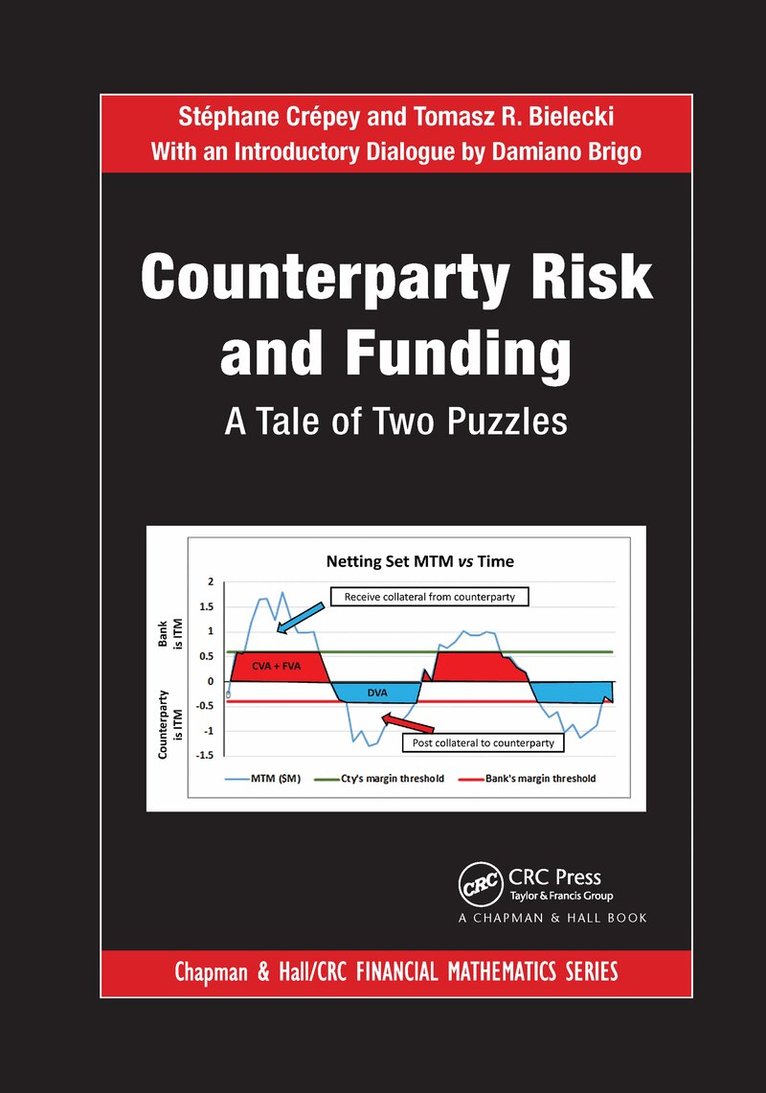

Solve the DVA/FVA Overlap Issue and Effectively Manage Portfolio Credit Risk

Counterparty Risk and Funding: A Tale of Two Puzzles explains how to study risk embedded in financial transactions between the bank and its counterparty. The authors provide an analytical basis for the quantitative methodology of dynamic valuation, mitigation, and hedging of bilateral counterparty risk on over-the-counter (OTC) derivative contracts under funding constraints. They explore credit, debt, funding, liquidity, and rating valuation adjustment (CVA, DVA, FVA, LVA, and RVA) as well as replacement cost (RC), wrong-way risk, multiple funding curves, and collateral.

The first part of the book assesses today’s financial landscape, including the current multi-curve reality of financial markets. In mathematical but model-free terms, the second part describes all the basic elements of the pricing and hedging framework. Taking a more practical slant, the third part introduces a reduced-form modeling approach in which the risk of default of the two parties only shows up through their default intensities. The fourth part addresses counterparty risk on credit derivatives through dynamic copula models. In the fifth part, the authors present a credit migrations model that allows you to account for rating-dependent credit support annex (CSA) clauses. They also touch on nonlinear FVA computations in credit portfolio models. The final part covers classical tools from stochastic analysis and gives a brief introduction to the theory of Markov copulas.

The credit crisis and ongoing European sovereign debt crisis have shown the importance of the proper assessment and management of counterparty risk. This book focuses on the interaction and possible overlap between DVA and FVA terms. It also explores the particularly challenging issue of counterparty risk in portfolio credit modeling. Primarily for researchers and graduate students in financial mathematics, the book is also suitable for financial quants, managers in banks, CVA desks, and members of supervisory bodies.

935 kr

Läs direkt efter köp

Solve the DVA/FVA Overlap Issue and Effectively Manage Portfolio Credit Risk

Counterparty Risk and Funding: A Tale of Two Puzzles explains how to study risk embedded in financial transactions between the bank and its counterparty. The authors provide an analytical basis for the quantitative methodology of dynamic valuation, mitigation, and hedging of bilateral counterparty risk on over-the-counter (OTC) derivative contracts under funding constraints. They explore credit, debt, funding, liquidity, and rating valuation adjustment (CVA, DVA, FVA, LVA, and RVA) as well as replacement cost (RC), wrong-way risk, multiple funding curves, and collateral.

The first part of the book assesses today’s financial landscape, including the current multi-curve reality of financial markets. In mathematical but model-free terms, the second part describes all the basic elements of the pricing and hedging framework. Taking a more practical slant, the third part introduces a reduced-form modeling approach in which the risk of default of the two parties only shows up through their default intensities. The fourth part addresses counterparty risk on credit derivatives through dynamic copula models. In the fifth part, the authors present a credit migrations model that allows you to account for rating-dependent credit support annex (CSA) clauses. They also touch on nonlinear FVA computations in credit portfolio models. The final part covers classical tools from stochastic analysis and gives a brief introduction to the theory of Markov copulas.

The credit crisis and ongoing European sovereign debt crisis have shown the importance of the proper assessment and management of counterparty risk. This book focuses on the interaction and possible overlap between DVA and FVA terms. It also explores the particularly challenging issue of counterparty risk in portfolio credit modeling. Primarily for researchers and graduate students in financial mathematics, the book is also suitable for financial quants, managers in banks, CVA desks, and members of supervisory bodies.

Credit Risk Frontiers

Subprime Crisis, Pricing and Hedging, CVA, MBS, Ratings, and Liquidity

672 kr

Skickas inom 5-8 vardagar

1 558 kr

Skickas inom 5-8 vardagar

1 891 kr

Läs direkt efter köp

The 2nd edition of this successful book has several new features. The calibration discussion of the basic LIBOR market model has been enriched considerably, with an analysis of the impact of the swaptions interpolation technique and of the exogenous instantaneous correlation on the calibration outputs. A discussion of historical estimation of the instantaneous correlation matrix and of rank reduction has been added, and a LIBOR-model consistent swaption-volatility interpolation technique has been introduced.

The old sections devoted to the smile issue in the LIBOR market model have been enlarged into several new chapters. New sections on local-volatility dynamics, and on stochastic volatility models have been added, with a thorough treatment of the recently developed uncertain-volatility approach. Examples of calibrations to real market data are now considered.

The fast-growing interest for hybrid products has led to new chapters. A special focus here is devoted to the pricing of inflation-linked derivatives.

The three final new chapters of this second edition are devoted to credit. Since Credit Derivatives are increasingly fundamental, and since in the reduced-form modeling framework much of the technique involved is analogous to interest-rate modeling, Credit Derivatives -- mostly Credit Default Swaps (CDS), CDS Options and Constant Maturity CDS - are discussed, building on the basic short rate-models and market models introduced earlier for the default-free market. Counterparty risk in interest rate payoff valuation is also considered, motivated by the recent Basel II framework developments.

1 140 kr

Läs direkt efter köp

The 2nd edition of this successful book has several new features. The calibration discussion of the basic LIBOR market model has been enriched considerably, with an analysis of the impact of the swaptions interpolation technique and of the exogenous instantaneous correlation on the calibration outputs. A discussion of historical estimation of the instantaneous correlation matrix and of rank reduction has been added, and a LIBOR-model consistent swaption-volatility interpolation technique has been introduced.

The old sections devoted to the smile issue in the LIBOR market model have been enlarged into several new chapters. New sections on local-volatility dynamics, and on stochastic volatility models have been added, with a thorough treatment of the recently developed uncertain-volatility approach. Examples of calibrations to real market data are now considered.

The fast-growing interest for hybrid products has led to new chapters. A special focus here is devoted to the pricing of inflation-linked derivatives.

The three final new chapters of this second edition are devoted to credit. Since Credit Derivatives are increasingly fundamental, and since in the reduced-form modeling framework much of the technique involved is analogous to interest-rate modeling, Credit Derivatives -- mostly Credit Default Swaps (CDS), CDS Options and Constant Maturity CDS - are discussed, building on the basic short rate-models and market models introduced earlier for the default-free market. Counterparty risk in interest rate payoff valuation is also considered, motivated by the recent Basel II framework developments.

648 kr

Skickas inom 5-8 vardagar

1 513 kr

Skickas inom 10-15 vardagar