Structured Dependence between Stochastic Processes

AvTomasz R. Bielecki,Jacek Jakubowski

Inbunden, Engelska, 2020

Del 175 i serien Encyclopedia of Mathematics and its Applications

1 621 kr

Beställningsvara. Skickas inom 7-10 vardagar. Fri frakt över 249 kr.

Beskrivning

The relatively young theory of structured dependence between stochastic processes has many real-life applications in areas including finance, insurance, seismology, neuroscience, and genetics. With this monograph, the first to be devoted to the modeling of structured dependence between random processes, the authors not only meet the demand for a solid theoretical account but also develop a stochastic processes counterpart of the classical copula theory that exists for finite-dimensional random variables. Presenting both the technical aspects and the applications of the theory, this is a valuable reference for researchers and practitioners in the field, as well as for graduate students in pure and applied mathematics programs. Numerous theoretical examples are included, alongside examples of both current and potential applications, aimed at helping those who need to model structured dependence between dynamic random phenomena.

Produktinformation

Utforska kategorier

Mer om författaren

Recensioner i media

Innehållsförteckning

Hoppa över listan

Mer från samma författare

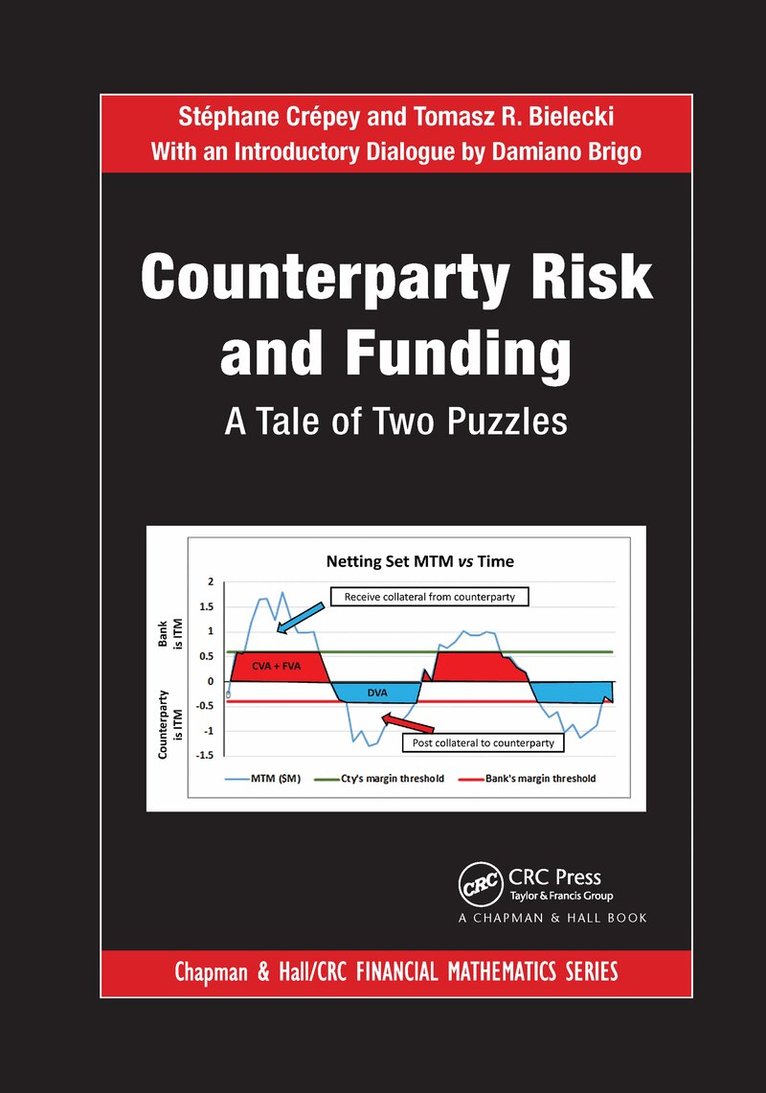

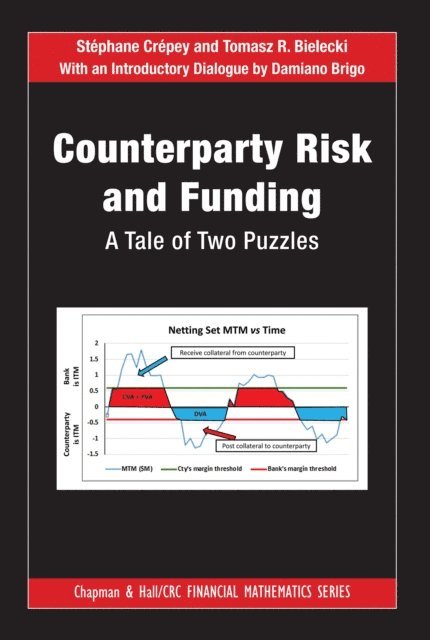

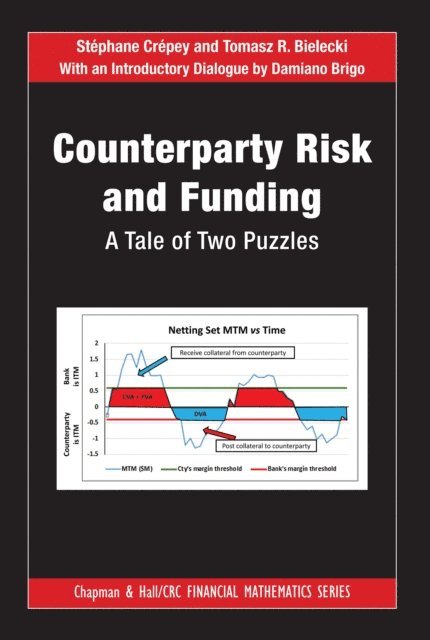

Counterparty Risk and Funding

Stéphane Crépey, Tomasz R. Bielecki, Damiano Brigo

Inbunden, 2014

3 043 kr

Del 1847

Paris-Princeton Lectures on Mathematical Finance 2003

Tomasz R. Bielecki, Tomas Björk, Monique Jeanblanc, Marek Rutkowski, Jose A. Scheinkman, Wei Xiong, René Carmona, Erhan Çınlar, Ivar Ekeland, Elyès Jouini, Jose A. Scheinkman, Nizar Touzi

Häftad, 2004

492 kr

Stochastic Methods in Finance

Kerry Back, Tomasz R. Bielecki, Christian Hipp, Shige Peng, Walter Schachermayer, Marco Frittelli, Wolfgang J. Runggaldier

Häftad, 2004

546 kr

Paris-Princeton Lectures on Mathematical Finance 2003

Wei Xiong, Jose A. Scheinkman, Marek Rutkowski, Monique Jeanblanc, Tomas Bjork, Tomasz R. Bielecki, Nizar Touzi, Jose A. Scheinkman, Elyes Jouini, Ivar Ekeland, Erhan Cinlar, Rene Carmona

E-bok

2004633 kr

Stochastic Methods in Finance

Walter Schachermayer, Shige Peng, Christian Hipp, Tomasz R. Bielecki, Kerry Back, Wolfgang J. Runggaldier, Marco Frittelli

E-bok

2004712 kr

Credit Risk: Modeling, Valuation and Hedging

Tomasz R. Bielecki, Marek Rutkowski

Inbunden, 2001

1 300 kr

Hoppa över listan

Mer från samma serie

Del 71

Del 86

Del 70

Del 66

Del 41

Del 72

Del 50

Del 51

Handbook of Categorical Algebra: Volume 2, Categories and Structures

Francis Borceux

Häftad, 2008

1 191 kr

Del 52

Del 76

Hoppa över listan

Du kanske också är intresserad av

Del 1847

Paris-Princeton Lectures on Mathematical Finance 2003

Tomasz R. Bielecki, Tomas Björk, Monique Jeanblanc, Marek Rutkowski, Jose A. Scheinkman, Wei Xiong, René Carmona, Erhan Çınlar, Ivar Ekeland, Elyès Jouini, Jose A. Scheinkman, Nizar Touzi

Häftad, 2004

492 kr

Stochastic Methods in Finance

Kerry Back, Tomasz R. Bielecki, Christian Hipp, Shige Peng, Walter Schachermayer, Marco Frittelli, Wolfgang J. Runggaldier

Häftad, 2004

546 kr

Credit Risk: Modeling, Valuation and Hedging

Tomasz R. Bielecki, Marek Rutkowski

Inbunden, 2001

1 300 kr

Stochastic Methods in Finance

Walter Schachermayer, Shige Peng, Christian Hipp, Tomasz R. Bielecki, Kerry Back, Wolfgang J. Runggaldier, Marco Frittelli

E-bok

2004712 kr

Paris-Princeton Lectures on Mathematical Finance 2003

Wei Xiong, Jose A. Scheinkman, Marek Rutkowski, Monique Jeanblanc, Tomas Bjork, Tomasz R. Bielecki, Nizar Touzi, Jose A. Scheinkman, Elyes Jouini, Ivar Ekeland, Erhan Cinlar, Rene Carmona

E-bok

2004633 kr